Updating your browser will give you an optimal website experience. Learn more about our supported browsers.

Managing Investment Risk

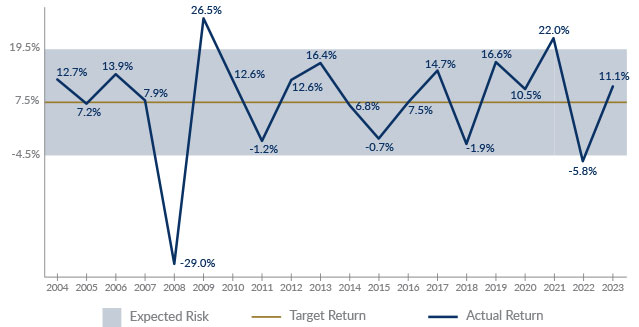

Risk is a factor in any investment, and we manage risk very closely. Fortunately, we have a great track record of meeting our performance goals.

We know we’re not going to achieve our long-term goal every year — some years our portfolio will return more, and other years it will earn less, depending on markets.

So what’s an acceptable level of risk? For us, it’s the smallest amount of risk we can take to achieve our long-term return goal.

What is risk?

When making investment decisions, there are two kinds of risk the TCDRS Board of Trustees must be aware of:

-

Long-term risk is the possibility that investment return will not be sufficient to grow our assets enough to pay future benefit claims.

-

Short-term risk is the possibility of varying returns from year-to-year. Higher returning asset classes tend to be more volatile (or risky) than lower returning asset classes. While their return over longer timeframes may be higher, their year-to-year return will fluctuate more widely.

As a result, our approach to investment risk centers around two main questions:

-

Is our portfolio designed to earn enough in returns combined with employer and employee contributions to pay the retirement benefits promised by our employers? (This is long-term risk.)

-

Are we comfortable with the potential year-to-year volatility in returns from our current mix of investments and its impact on employer rates? (This is short-term risk.)

Diversification is our primary defense against both long-term and short-term risk.

Investment risk and employer rates

Annual investment returns have a direct impact on employer plan rates because our employers are required by law to pay 100% of their required rate each year. A poor performing year could cause employer rates to increase for the following year.

That’s why we manage risk very closely. Fortunately, we have a great track record of meeting (and exceeding) our performance goals. In addition to managing risk in our portfolio, there are other strategies that both TCDRS and employers can use to keep rates stable.

How we do it: The nuts and bolts

Each year the board sets the risk tolerance of the total portfolio when adopting the investment return assumptions for each asset class. For every major asset class we’ve chosen for our portfolio, we expect a certain return and a certain amount of volatility. We use statistical tools, such as standard deviation and correlation, to evaluate asset classes and determine which fit best in our portfolio. While the range of volatility for individual asset classes may extend beyond the adopted risk tolerance, the risk of the entire portfolio is expected to remain within acceptable levels.

The gray bar in the graph above represents the amount of risk our portfolio is designed to operate within — a range of +/-12% centered around our long-term investment goal.

Related Content

Get more information on why TCDRS is a model plan when it comes to retirement.

Keeping Investment Costs Low

Our large fund size creates unique economies of scale that make our investment process more efficient. We never charge fees to our pa...

Read more

Responsible Guidance for Investments

The TCDRS Board of Trustees is responsible for overseeing the investment of TCDRS assets. They receive assistance from the investment...

Read more

TCDRS Investment Managers

At TCDRS, we’re proud to work with industry-leading investment managers to help manage our assets.

Read more