Updating your browser will give you an optimal website experience. Learn more about our supported browsers.

Set Yourself Up for Investment Success

Saving for retirement is a long-term endeavor. One way you can help increase your financial security in retirement is to have additional retirement savings accounts.

By Leah Golden

Some employers offer 401(k)s or 457s to help their employees save extra. You can also contact a bank or investment company to open an Individual Retirement Account (IRA) on your own.

However, there are a few things you should do before you start socking away extra for retirement.

-

Pay down debt first.

Because of interest rates, debts can cost you more than the money you borrowed. Paying down your debts — especially those with high interest rates — can save you a lot of money. The faster you pay down your debts, the less interest you pay. The less interest you pay, the more money you have for investing. Win-win. -

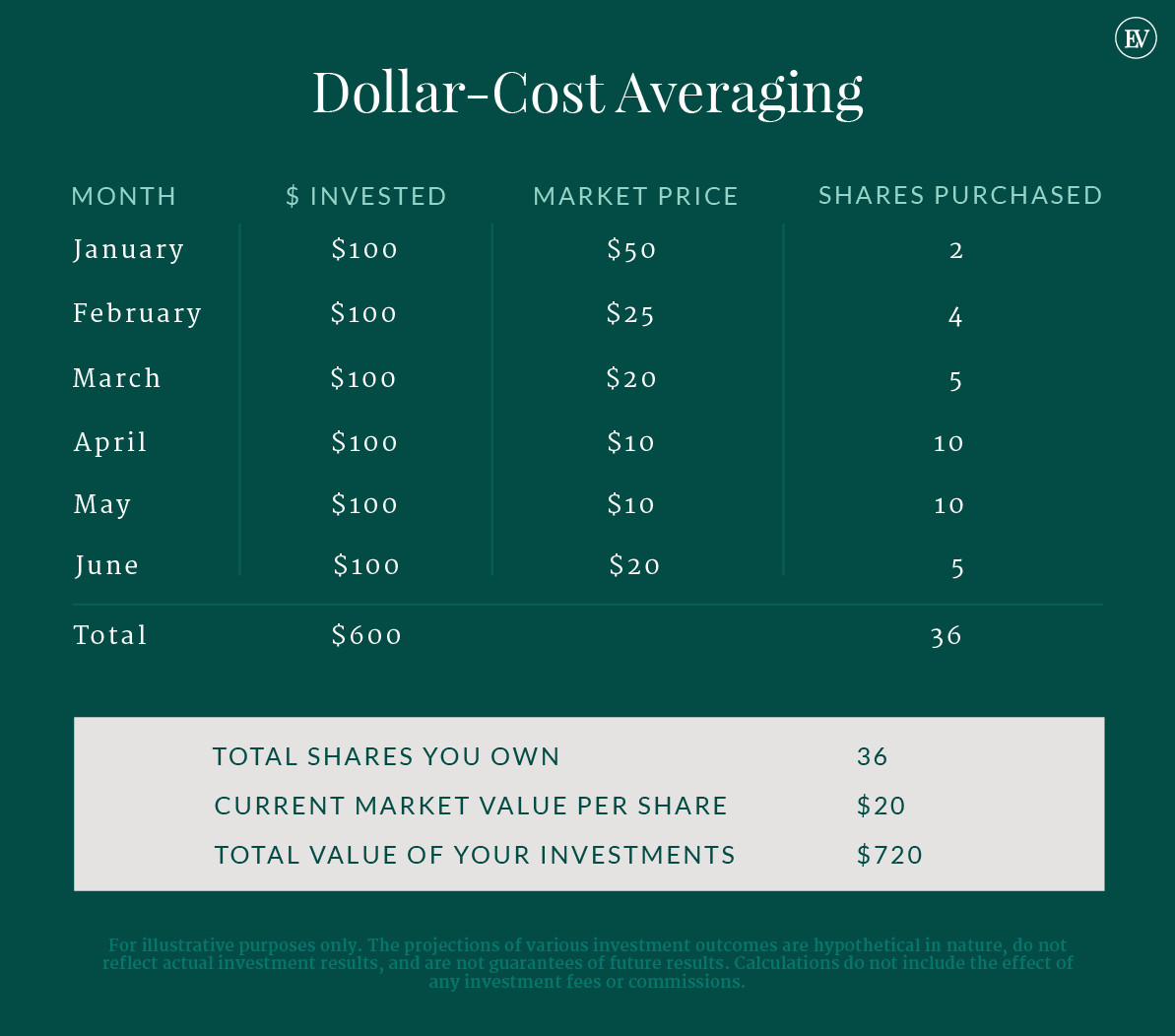

Plan to invest regularly.

When you invest a little bit each month, you reap the benefits of dollar-cost averaging. “Dollar-cost averaging” means investing the same amount of money at regular intervals no matter what the market is doing. That last part is important. (This table will show you how it works.) -

Ask about fees.

IRAs and accounts like them come with fees. All kinds of fees. Before you invest your money, ask any investment company you’re considering about what fees are associated with the retirement account you want to open.

You can also ask about lower-fee options from the company you’re considering or shop around. Higher fees don’t necessarily mean better investment performance. Reducing your investment fees can help you build a more financially secure retirement. You have a right to know where your money will go before you start investing.

{kind=link}

Related Content

Get more information on why TCDRS is a model plan when it comes to retirement.

08.06.2021

Downsizing? Improve Your Home’s Value First

Cost-effective ways to increase your home’s value before putting it on the market.

Read more

08.09.2021

Is it Safe to Take Those Facebook Quizzes?

Many of the personality quizzes you see on Facebook and other social media platforms are actually data collection scams posted by fra...

Read more

04.20.2022

Working in Retirement: The Red Flags and Green Lights of Remote Jobs

Work-from-home jobs are often great options for retirees looking to stay busy and supplement their retirement benefit. But how do you...

Read more