Updating your browser will give you an optimal website experience. Learn more about our supported browsers.

Account Portability

You don’t have to withdraw your account just because you’re leaving your job. There are a lot of good reasons to leave your money in TCDRS.

With TCDRS, You Can Take it With You

Sometimes the road to retirement includes job changes, but leaving your county or district job doesn’t mean leaving your retirement savings behind.

Continuing to Earn Service Time

Even if you’re not vested when you leave your job, you may want to keep your money in TCDRS, in case you take a job with another TCDRS employer or a job covered by a proportionate retirement system, such as one for the state, a city or a school district. This will enable you to continue saving for your retirement while working for your new employer. You may even be able to count current — or past — military time you earn with your new employer toward your TCDRS retirement eligibility. See our Service Time page for more information.

Account Options

You don’t have to withdraw your account just because you’re leaving your job. There are a lot of good reasons to leave your money in TCDRS:

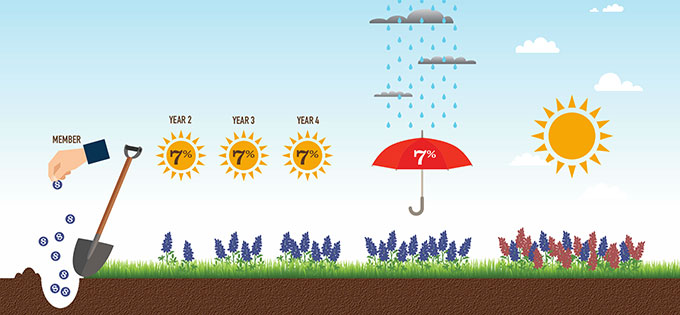

- Your account continues to grow at 7% compound interest.

- Upon retirement eligibility, you will receive a lifetime monthly benefit.

- If you’ve completed four years of service, you remain eligible for a Survivor Benefit.

- Watch this short video to learn more about your options.

Option 1: Keep Your Money in TCDRS

To keep your money in your TCDRS account, all you have to do is keep your account information up-to-date with us. We need your current address and your current beneficiary information.

Your money will earn interest for as long as you keep it in TCDRS.

You may also be able to count service time you earn with another TCDRS employer or from military service toward your retirement eligibility. If you work for the state, a city or a school, the time you earn in those retirement systems can also count. Our Service Time page can tell you more about your options.

Option 2: Roll Over Your Account

You can avoid paying taxes or penalties by rolling your money over into another tax-deferred retirement account. These accounts include traditional IRAs or your new employer's retirement plan (if it allows rollovers). However, you lose employer matching with any rollover and you forfeit your lifetime benefit.

You can apply for withdrawal when you sign into your online account. When you complete the application, choose the direct rollover option and provide the name of the plan or account into which you’re rolling your money.

We will send you a check made out to the financial institution you designate two to four weeks after we receive your application.

The following January, we will send you an IRS Form 1099-R detailing how much money you rolled over. You’ll need to file your 1099-R with your income tax return.

Option 3: Withdraw Your Account

If you choose to withdraw your money from TCDRS, you may want to check with a tax professional or the IRS first. Your withdrawal will be subject to a minimum 20% withholding for taxes, you may face a 10% withdrawal penalty at tax time and your withdrawal could significantly affect your income taxes.

In addition, withdrawing your TCDRS account means you lose employer matching and forfeit your lifetime benefit from that account.

To withdraw your money, sign into your TCDRS account online and complete the withdrawal process. You can also apply for withdrawal over the phone by calling TCDRS Member Services at 800-823-7782.

We will send you a payment for the total amount of your account balance, minus the tax withholding, within 10 days of receiving your application.

The following January, we will send you an IRS Form 1099-R detailing how much money you withdrew and any taxes you withheld. You’ll need to file your 1099-R with your income tax return.

Related Content

Get more information on why TCDRS is a model plan when it comes to retirement.

3-Minute Retirement Checkup

It starts with a visit to our benefit payment estimator.

Read more

How Your TCDRS Savings Grow

Your retirement savings earn 7% compound interest each year, regardless of the economy. Reliability is a big deal when it comes to sa...

Read more

04.29.2021

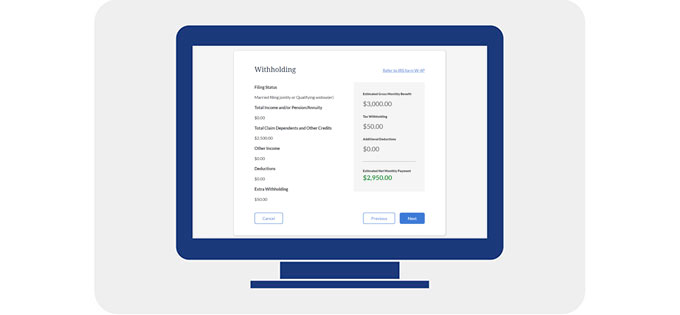

Change Your Withholding Anytime at TCDRS.org

The payment you receive every month from TCDRS counts as income, and you have to take it into account when filing your income taxes. ...

Read more